The economic outlook continues to improve for Australia. Most recently, both the government and the Central Bank released five-year growth forecasts, both of which show a modest recovery in 2010. “By 2011-12, the commodity-rich economy will again be firing on all cylinders with growth of 4.5%, well above the long-term growth rate of around 3%.”

This positive development coincided with the release of similarly upbeat economic data: “Retail sales surged 2.2 percent in March from the previous month, four times as much as economists forecast. Home-loan approvals jumped 4.9 percent, the sixth consecutive gain.” Meanwhile, unemployment shrank for the first time in months, and consumer confidence is once again rising. While the economy is forecast to shrink by .75% in the current fiscal year, this compares favorably with other industrialized countries.

The sudden turnaround can be attributed to a couple factors. First of all, the pickup in China’s economy is stimulating demand for natural resources, which had been slack for the last year. If not for simultaneously falling commodity prices, Australia might have even achieved positive economic growth for the year.

The government’s stimulus plan and spending initiatives have also played a role, although the extent cannot be measured accurately for a few months. “The government claims that measures in its budget will inject a further A$8.8 billion into the economy in 2009-10, adding to around A$50 billion in fiscal measures already announced since October 2008.”

The outlook for the Australian Dollar, meanwhile, is not so rosy. The 425 basis points in cumulative rate cuts that the Royal Bank of Australia (RBA) effected over the last year have lowered the interest rate differential with other industrialized countries. While the RBA has indicated that it will pause before cutting rates further, interest rate futures reflect the expectation that rates will be lower twelve months from now. “Economists say the RBA is open to cutting interest rates again if consumer and business confidence appear threatened, but for now it is content to let monetary and fiscal stimulus measures take hold.”

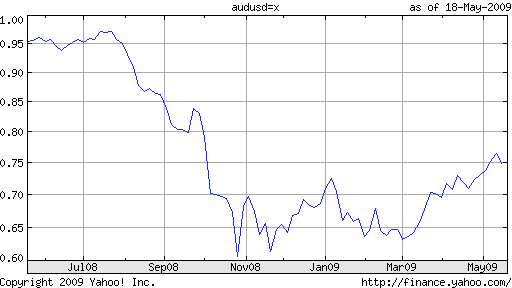

To be sure, the uptick in risk tolerance has been good for the Australian Dollar, igniting a 25% rise since March. The currency now stands at a 7-month high against the US Dollar. But the increasingly modest differential is now causing some analysts to question whether it is a reasonable risk to take, especially against the backdrop of volatility and a high correlation with global stock prices. “What’s the point of picking up a 3 percent interest-rate differential by being long Aussie and short Japan in a world where the exchange rate can move by that much in two days?” Asks One analyst rhetorically.

This same analyst is actually recommending investors to use the Australian Dollar as a funding currency, and go long on higher-yielding currencies, such as the Brazilian Real. This particular trade would have netted a respectable 5.9% return in 2009. How quickly the roles have reversed!

Deflation: Worst-Case Scenario or Already Here?

In following up on last week’s post (”Inflation or Stimulus: An In-depth Look At the Fed’s Response to the Credit Crisis“) on the possibility of inflation, I want to focus today’s post on the opposite phenomenon: deflation.

As evidenced by the huge expansion of government borrowing and Fed Quantitative easing, it is deflation which is currently the paramount concern of policymakers. While falling prices would seem to represent an ideal solution to the current economic downturn, deflation is actually quite pernicious if left unchecked. To elaborate: “When prices fall across the board, businesses and consumers postpone purchases because they expect lower prices later, or worry their incomes will decline or don’t want to acquire assets that will fall in value. Shrinking demand forces sellers to cut prices further, triggering a vicious cycle.” Deflation is also detrimental to consumers with liabilities, which remain the same even as incomes are falling.

Now that we understand what deflation looks like, let’s examine its likelihood. In fact, the current economic environment represents a perfect breeding ground for deflation. For example, both consumers and businesses are using stimulus and bailout checks to pay down debt, rather to increase spending. In addition, businesses are selling out of inventory rather than ramping up production, due to uncertainty for the future. Bond yields are rising, making it more expensive - and hence less likely - for companies to borrow and invest.

And what about the data? The Retail Price Index, “RPI - which turned negative for the first time in almost 50 years in March - is expected to fall from minus 0.4% to minus 1% in April.” The Consumer Price Index, meanwhile, “declined by 0.7 percent year-over-year in April, the largest 12-month drop since 1955.” It’s hard to take this data seriously, however, given the “seasonal adjustments” and “stripping of so-called volatile energy prices, and using the dubious ” ‘owners equivalent rent,’ OER, to measure consumer housing expenses” in order to conceal the actual decline in property values. In short, the actual decline is probably much worse, especiall given the steep drop in commodities from 2008.

At least Fed Chairman Ben Bernanke is satisfied, and was most recently quoted for his belief that “the risks of deflation were receding.” Bernanke remains committed to pumping money into the economy via its purchases of government bonds. It still has a ways to go in making good on its promise to buy more than $1 Trillion in securities.

While it’s easy to blame the Fed, it’s also hard not to begrudge it some sympathy for having to toe a very thin line between deflation and hyperinflation. In the event that its successful in forestalling a decline in prices, it will have just enough time to catch its breath before drawing all of the new money out of the economy so as to prevent inflation from taking hold and another bubble from forming in asset prices.

0 comments:

Post a Comment